When earthquakes strike, the damage is often more than what government disaster funds can cover. To address this, researchers have developed a new financial model that can help make earthquake catastrophe bonds more attractive to investors while ensuring better disaster preparedness.

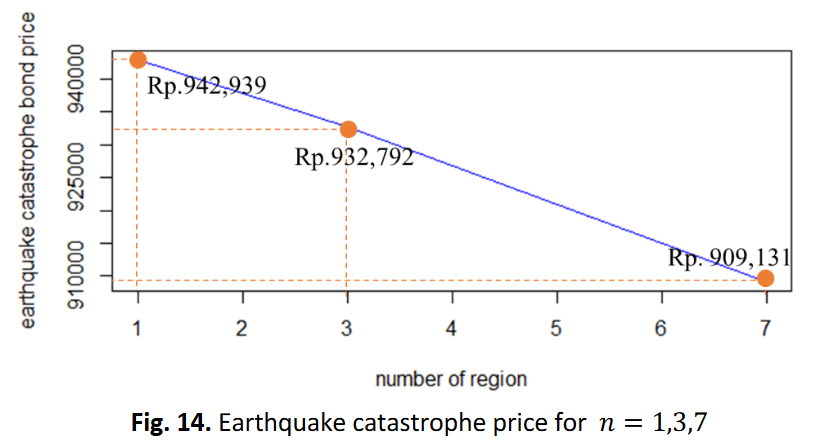

The study introduces the Decomposition of Disaster Region Using Earthquake Parameters and STDM Distance on Catastrophe Bond Pricing (DECBP) model. This approach evaluates earthquake-prone areas by analyzing magnitude, depth, and space-time-depth-magnitude (STDM) distance. By dividing regions based on seismic risk, the model provides a clearer and more transparent way to determine earthquake bond prices.

For investors, this model helps balance risks and returns by showing how factors like interest rates and coupon values affect bond prices. For governments, particularly in earthquake-prone areas like Indonesia, catastrophe bonds could become a vital tool to secure emergency funds before a disaster strikes.

The research highlights past events, such as the 7.3 magnitude earthquake in West Java, where losses exceeded available contingency funds. By applying catastrophe bonds through the proposed model, governments can build a stronger safety net while giving investors greater confidence in financing disaster risk reduction.

This innovation directly supports Sustainable Cities and Communities (SDG 11) by promoting resilience, financial preparedness, and sustainable disaster management strategies.

#EarthquakeBonds #DisasterRiskReduction #SustainableCities

Link to the paper: https://www.scopus.com/pages/publications/85191466646

23/Mat/2025