A team of researchers from Universitas Padjadjaran, Indonesia, including Yuliani Indrianingsih, Sukono, Sri Wulandari, and Eridani, in collaboration with Sardar M.N. Islam from Victoria University, Australia, has developed a new model for pricing earthquake catastrophe bonds (CAT bonds) using correlated dual trigger indices. The study introduces an approximate pricing solution powered by the Monte Carlo simulation algorithm.

The problem addressed in this paper is that conventional CAT bond pricing often relies on single triggers, which may not adequately capture the complex nature of earthquake risks. Single-index triggers can result in either investor losses or insurer dissatisfaction due to mismatches between payouts and actual damages.

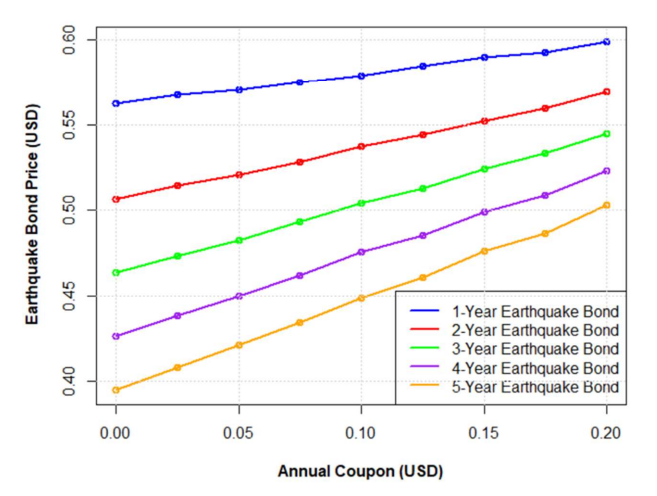

To overcome this, the authors designed a dual trigger index model that combines two correlated risk indices to more accurately reflect earthquake characteristics. Using Monte Carlo simulations, they approximate bond prices under varying correlation levels and risk thresholds. This approach enhances both fairness and transparency in the CAT bond market.

The study concludes that incorporating correlated dual triggers provides more robust and realistic pricing structures for CAT bonds. The Monte Carlo algorithm proves effective in delivering approximate solutions that balance computational efficiency with pricing accuracy.

This work directly contributes to the United Nations Sustainable Development Goals (SDGs):

- SDG 11 (Sustainable Cities and Communities): by improving disaster risk financing mechanisms to reduce urban vulnerability.

- SDG 13 (Climate Action): by supporting resilience against climate-related disasters and extreme seismic events.

- SDG 9 (Industry, Innovation and Infrastructure): by advancing innovative financial instruments for sustainable infrastructure planning.

- SDG 17 (Partnerships for the Goals): by showcasing international collaboration in financial mathematics and risk management.

Overall, the research highlights how advanced mathematical modeling and simulation can strengthen the global financial system’s ability to manage disaster risks and support sustainable development.

04/Mat/2025